Sachin Gupta

Sachin Gupta Ruchit Jain

Ruchit JainTop Growth Stocks Trading at a Discount

by

5paisa Research Team

4th Nov 2024

Last Updated: 15th December 2022 - 01:25 am

2021 was a year of Start-ups. We witnessed a record number of start-ups attaining the holy unicorn status in 2021. Not just that, we witnessed the record listing of these companies on Indian exchanges. Prior to 2021, investors in these companies were mainly VC/ Private investors, but for the first time these companies went public, and to say the least, investors went gaga over them.

In 2021, eight startups including Nykaa, Paytm, and Zomato together raised approximately $7 billion from investors. Most of them made a bumper debut, listed at a premium, and got insane valuations.

Exactly a year after, most of these companies are almost 50% down from listed prices. They have wiped off billions of dollars of investor money.

These start-ups are witnessing intense selling pressure as the lock-in period of pre-IPO investors end.

But, what went wrong? Why are these start-ups, that were once investor favorites

now losing their shine?

Zomato, Nykaa, and Paytm are all leaders in their respective segments, however, their path to profitability is still quite long and shady. Even now, most of them are just cash-burning companies and have not seen a dime in profits.

For instance, In 2021-22, Paytm’s parent company, One97 Communications, clocked Rs 5,264.3 crore in revenue 65% higher than the previous year, but at the same time, its losses widened by 41% and stood at Rs 2,396.4 crore.

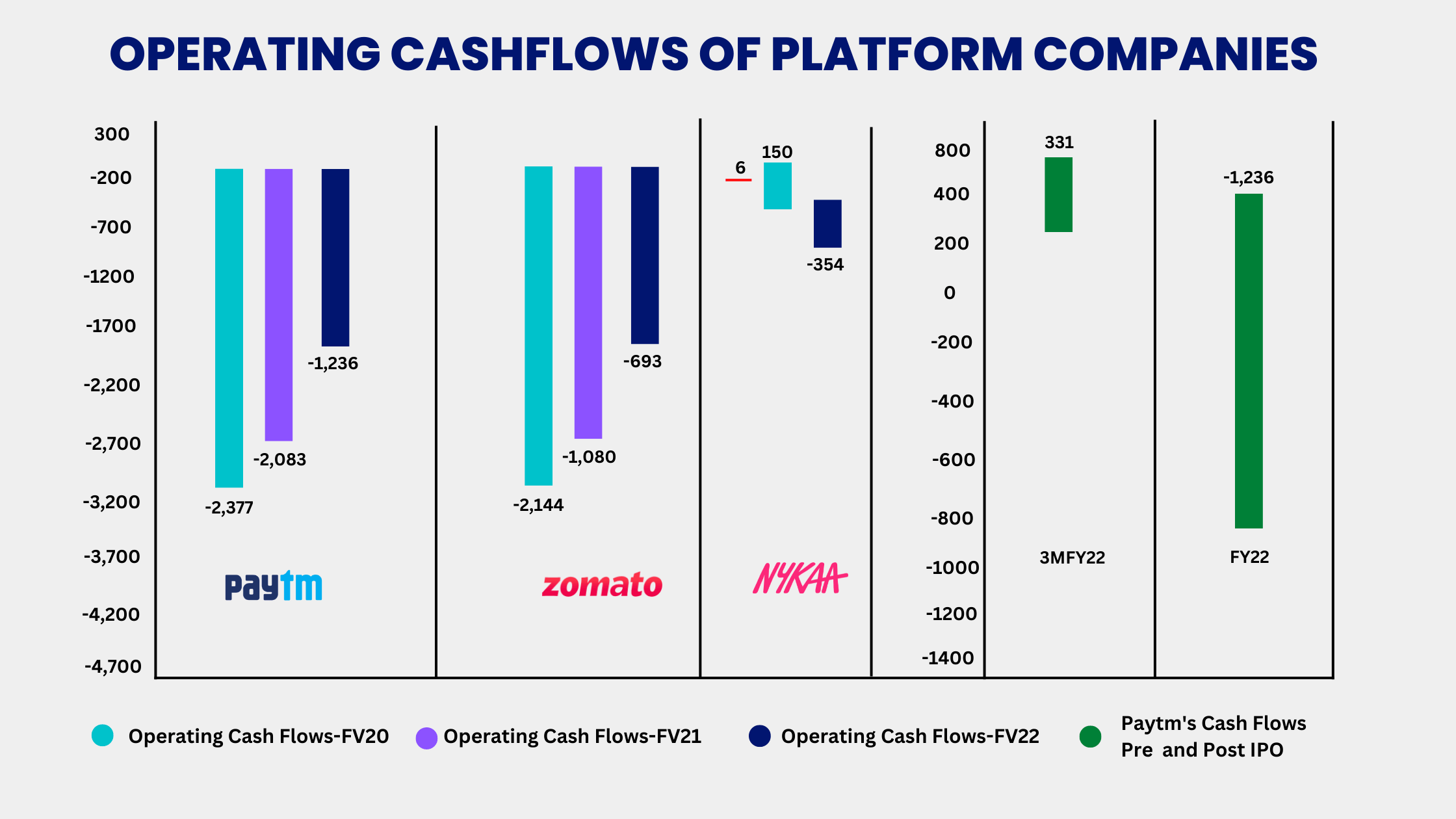

At the time of the listing, Paytm was the only start-up that had positive cashflows, but post its listing its cashflows have declined significantly.

Similarly, Nykaa, which was the only profitable start-up among the three, saw its

net profit fall from INR 62 crore in FY21 to INR 41 crore in FY22.

It also witnessed a steep decline in its cash flows. Its cash flow from operations was INR 134 crore in FY21, while it had a negative cash flow from operations of INR 354 crore in FY22.

Its EBITDA margins have also declined from 6% in FY21 to 4% in FY22. All in all the company is sacrificing profitability for growth.

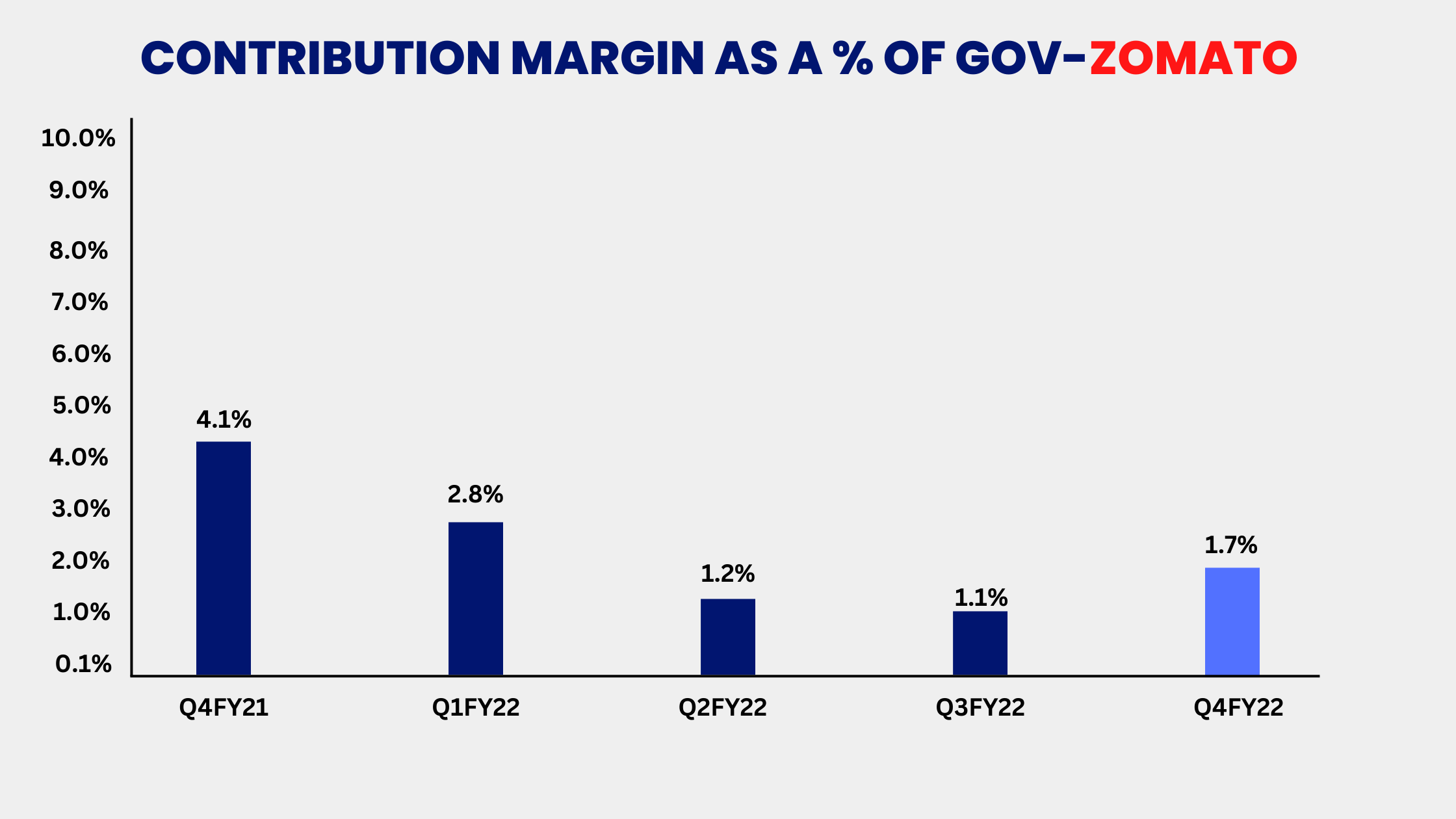

Lastly, we have Zomato, which is struggling to improve its contribution margin, it is the money it makes on each order after deducting all the costs.

Although its Gross order value, that is the total value of all orders in a given period has grown significantly in the last one year, the contribution margin has declined due to high fuel costs.

Its contribution margin fell from 4.1% in Q4 FY21 to 1.7% in Q4 FY22, this implies Zomato has not been able to pass on the additional costs to its consumers.

Even though all three have assured investors that they will improve their profitability and operational efficiency, their cash flow from operations has declined in the first half of 2023 compared to last year.

Investors aren’t really optimistic about their performance in the coming years, because these companies are still burning billions of dollars to run their operations and if it goes on like this, they will have to raise additional capital through equity or debt, which will either dilute the shareholding of existing investors or increase the interest burden on the company.

Also, after the interest rate hikes in the US, investors are fearing a recession and a slowdown in the demand for the products. All in all, amidst an uncertain economic climate, investors prefer companies with strong balance sheets and cash reserves rather than cash-burning start-ups that promise high growth.

Trending on 5paisa

04

5paisa Research Team

5paisa Research Team

Discover more of what matters to you.

Indian Stock Market Related Articles

Top Growth Stocks Trading at a Discount

Top 10 Best Government Bonds in India

Muhurat Trading 2024: Expert Tips and Strategies for Diwali Success

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. For detailed disclaimer please Click here.

Want to Use 5paisa

Trading App?