5paisa Research Team

5paisa Research Team

Sachin Gupta

Sachin Gupta

Multibaggers Penny Stocks For 2025

by

5paisa Research Team

6th Jan 2025

Last Updated: 13th December 2023 - 09:36 am

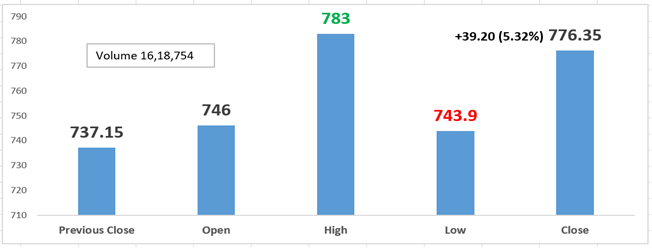

Movement of the Day

Analysis

1. Strengths - Strong Momentum: Price above short, medium and long term Simple Moving Averages from 5 days to 200 days respectively.

2. Weaknesses - Promoters increased pledged shares QoQ

1. ONE Can like Century for its robust franchise (distribution throughout India, active marketing, and a large selection of SKUs), leading position in the majority of wood sectors, increases in market share, and solid return ratios.

2. Revenue increased 10% YoY in Q2FY24, driven primarily by robust growth in the MDF (+26% YoY, helped by brownfield development in Punjab) and ply (+11% YoY) categories. Due to poor performance in the laminate and particle board categories, EBITDA fell 15% year over year.

3. Due to decreased EBITDA, increased capital costs, and tax outflow, APAT decreased 31% year over year. All of its segments are operating according to their capex plan.

1. Revenue Growth: Q2FY24 witnessed a 10% YoY revenue increase, propelled by a robust 26% surge in Medium Density Fiberboard (MDF), supported by the Hoshiyarpur ramp-up, and an 11% rise in the plywood segments. However, laminates and particle board revenues declined 3% and 19% YoY, respectively, due to subdued demand.

2. Volume Dynamics: Ply, laminates, and MDF volumes exhibited positive YoY growth at 8%, 7%, and 19%, respectively, while particle board volumes declined by 4%.

3. EBITDA Performance: EBITDA experienced a 15% YoY decline, primarily attributed to weaker performance in laminates and particle board segments. Segmental EBITDA for ply and MDF demonstrated resilience with a 5% and 24% YoY rise, reaching INR 718 million and INR 520 million, respectively. Conversely, laminates and particle board segmental EBITDA declined by 4% and 37% YoY, totalling INR 192 million and INR 86 million, respectively.

4. Margin Analysis: On a YoY basis, all segments reported lower margins, while on a QoQ basis, ply and particle board margins remained relatively stable. Notably, MDF margins recovered by 100bps QoQ, attributed to operational leverage gains and the ramp-up of the Punjab plant. Laminates margin expanded by 200bps QoQ to 11.2%, recovering from a lower base.

5. APAT Decline: The Adjusted Profit After Tax (APAT) declined, reflecting the impact of lower EBITDA, higher capital charges, and increased tax outgo, indicating challenges in sustaining profitability during the quarter.

(Source:SImplyWS)

Analysis

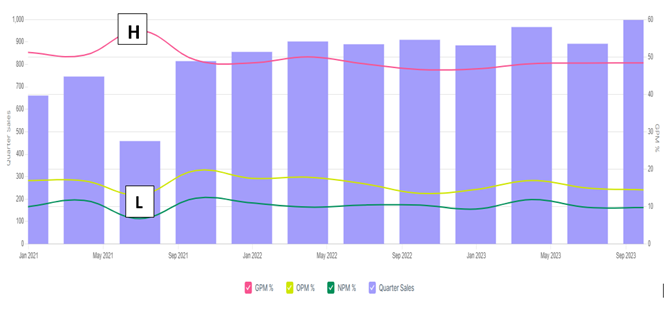

1. Operational Efficiency: A rising operating profit margin suggests that the company is managing its operating expenses effectively in relation to its revenue. This can be an indication of efficient day-to-day operations.

2. Profitability Growth: Increasing net profit margin indicates that the company is not only generating more revenue but also keeping a larger proportion of it as net profit. This could result from improved cost controls, increased sales, or better pricing strategies.

3. Gross Profitability: A rising gross profit margin indicates that the company is effectively managing its production costs. This could be attributed to factors such as economies of scale, negotiating better deals with suppliers, or optimizing manufacturing processes.

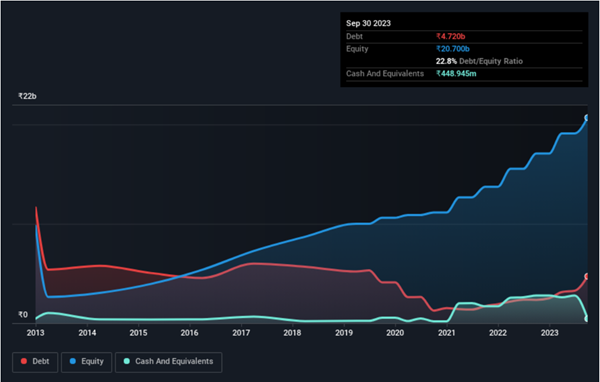

Strategic Expansions: Century plans a significant INR 10.5/4.5 billion Capex in FY24/FY25E for ongoing expansions, including doubling MDF capacity in AP, laminates expansion, particle board expansion in Chennai, and plywood expansions in Hoshiarpur.

Revenue Growth Guidance: Management projects a 10% ply revenue growth in H2FY24, targeting ~13-14% Operating Profit Margin (OPM). In MDF, a robust 25%+ YoY growth is anticipated in H2FY24, supported by the Hoshiarpur ramp-up, with an emphasis on maintaining stable/better margins.

Segmental Improvement: Expectations for improved revenue and OPM in the laminate and particle board segments in the coming quarters signal positive momentum, reflecting management's strategic initiatives and market dynamics.

Earnings Revision: Factoring in the guidance, FY24E Earnings Per Share (EPS) is revised upward by +3%, demonstrating confidence in the company's growth trajectory. However, FY25 EPS is maintained.

Target Price Unchanged: Despite the earnings revision, the unchanged Target Price of INR 745/sh indicates a steady outlook, possibly reflecting a balanced consideration of growth prospects and market conditions. Investors may view this as a signal of stability and sustained performance.

Indian Stock Market Related Articles

Multibaggers Penny Stocks For 2025

Top New Year Stock Picks for 2025: Best Investment Opportunities

Top Energy ETFs in India - Best Funds to Invest

Top 5 Nifty 50 ETFs in India by Returns

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. For detailed disclaimer please Click here.