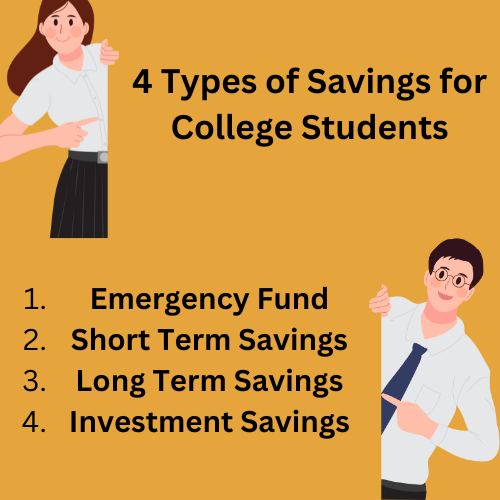

College is a crucial time to establish good financial habits, and building different types of savings can provide a strong foundation for future financial stability. Here are four essential types of savings every college student should consider: an emergency fund to cover unexpected expenses, short-term savings for upcoming costs like textbooks and trips, long-term savings for future goals such as studying abroad or buying a car, and retirement savings to ensure financial security in later years. Each type of savings serves a unique purpose and helps students manage their finances effectively while planning for their future.

Emergency Fund

An emergency fund is a dedicated savings account designed to cover unexpected expenses or financial emergencies. This could include medical bills, car repairs, sudden travel expenses, or any other unforeseen costs. Having an emergency fund ensures that you have a financial cushion to fall back on, reducing the need to rely on credit cards or loans.

Importance of an Emergency Fund:

- Financial Security: An emergency fund provides a safety net, offering peace of mind that you can handle unexpected expenses without compromising your financial stability.

- Avoiding Debt: By having funds set aside for emergencies, you can avoid accumulating debt from credit cards or loans, which often come with high-interest rates.

- Stress Reduction: Knowing that you have a financial buffer can reduce stress and anxiety associated with unexpected financial challenges.

How Much to Save: Financial experts generally recommend saving at least 3-6 months’ worth of living expenses in your emergency fund. For college students, this amount can be adjusted based on individual circumstances, such as part-time job income, parental support, and monthly expenses.

Building Your Emergency Fund:

- Start Small: Begin by setting aside a small amount from your monthly income, such as ₹20-₹50, and gradually increase this amount over time.

- Automate Savings: Set up automatic transfers from your checking account to your emergency fund to ensure consistent contributions.

- Reduce Non-Essential Spending: Identify areas where you can cut back on non-essential spending and redirect those funds to your emergency fund.

- Utilize Windfalls: Allocate any unexpected income, such as tax refunds, bonuses, or monetary gifts, to your emergency fund.

Maintaining Your Emergency Fund:

- Accessibility: Keep your emergency fund in a high-yield savings account that offers easy access and earns interest over time.

- Replenish After Use: If you need to use your emergency fund, make it a priority to replenish the amount as soon as possible.

- Avoid Temptations: Use your emergency fund strictly for emergencies and resist the temptation to dip into it for non-essential expenses.

Short-Term Savings

Short-term savings are funds set aside for expenses you anticipate incurring within the next year. These could include costs for events like a spring break trip, new textbooks, holiday gifts, or a special occasion. Having a dedicated short-term savings account helps you manage these costs without relying on credit or loans.

Importance of Short-Term Savings:

- Financial Planning: Short-term savings allow you to plan for upcoming expenses and avoid last-minute financial stress.

- Avoiding Debt: By saving for short-term goals, you can avoid taking on debt to cover these expenses.

- Budgeting Practice: Setting and achieving short-term savings goals can help you develop good budgeting and financial management habits.

Setting Short-Term Savings Goals:

- Identify Upcoming Expenses: Make a list of expenses you anticipate over the next year, such as travel, school supplies, or special events.

- Estimate Costs: Estimate the cost of each expense and set a specific savings goal for each one.

- Create a Timeline: Determine when you will need the funds and create a savings timeline to ensure you reach your goal in time.

Strategies for Building Short-Term Savings:

- Monthly Contributions: Set aside a portion of your monthly income for short-term savings. Even small amounts can add up over time.

- Savings Challenges: Participate in savings challenges, such as the 52-week savings challenge, to make saving more engaging and fun.

- Utilize Savings Apps: Use budgeting and savings apps that can help you track your progress and stay motivated.

- Cut Back on Discretionary Spending: Identify areas where you can reduce discretionary spending, such as dining out or entertainment, and redirect those funds to your short-term savings.

Long-Term Savings

Long-term savings are funds set aside for future goals that are a few years away. These could include goals such as studying abroad, buying a car, or starting a postgraduate program. Long-term savings require consistent contributions and a disciplined approach to ensure that you achieve your financial objectives over time.

Importance of Long-Term Savings:

- Future Planning: Long-term savings help you plan for significant financial goals and ensure that you have the funds needed when the time comes.

- Financial Independence: Saving for long-term goals can provide financial independence and reduce reliance on loans or financial assistance from others.

- Goal Achievement: Setting and working toward long-term savings goals can give you a sense of accomplishment and motivation to achieve other financial objectives.

Setting Long-Term Savings Goals:

- Identify Your Goals: Determine what you want to achieve with your long-term savings, such as studying abroad, purchasing a vehicle, or funding further education.

- Estimate Costs: Research and estimate the costs associated with each goal to set a specific savings target.

- Create a Savings Plan: Develop a savings plan that outlines how much you need to save each month to reach your goal within the desired timeframe.

Strategies for Building Long-Term Savings:

- Consistent Contributions: Make regular contributions to your long-term savings account, even if the amounts are small. Consistency is key to building a substantial savings fund.

- Automate Savings: Set up automatic transfers to your long-term savings account to ensure regular contributions without needing to think about it.

- Invest Wisely: Consider investing a portion of your long-term savings in low-risk investment options, such as mutual funds or fixed deposits, to earn higher returns over time.

- Track Your Progress: Regularly monitor your savings progress and make adjustments to your plan as needed to stay on track.

Investment Savings

Investment savings involve setting aside funds to invest in various financial instruments such as stocks, bonds, mutual funds, or exchange-traded funds (ETFs). These investments can provide higher returns over the long term compared to traditional savings accounts.

Importance of Investment Savings:

- Wealth Growth: Investments have the potential to grow significantly over time, helping you build wealth and achieve financial goals.

- Beat Inflation: Investments can offer returns that outpace inflation, ensuring your money retains its purchasing power.

- Diversification: By investing in a mix of assets, you can diversify your portfolio and spread risk.

Starting Investment Savings:

- Research: Educate yourself about different investment options and their associated risks and returns.

- Start Small: Begin with a small amount of money and gradually increase your investments as you become more comfortable.

- Diversify: Spread your investments across various asset classes to minimize risk.

Conclusion

Balancing these different types of savings can help college students manage their finances more effectively and achieve their financial goals while in college. By establishing an emergency fund, setting aside short-term and long-term savings, and starting to save for retirement early, students can create a solid financial foundation that will serve them well throughout their lives. Each type of savings serves a unique purpose, and together, they contribute to a comprehensive and well-rounded financial strategy.