Mutual funds have long been one of the most popular investment options for individuals seeking diversification and professional management without directly delving into the complexities of the stock market. They are often marketed as a convenient, low-cost way for investors to achieve their financial goals. However, beneath the surface of their apparent simplicity lie a series of hidden costs that may be eroding your returns without your full awareness. These costs, often embedded in the fund structure and operations, can significantly impact your wealth over time. Are you unknowingly paying more than you think for your mutual fund investments? Let’s dive deeper into the world of mutual funds to uncover the hidden costs and their implications.

Expense Ratios: The Ongoing Drain on Your Returns

The most well-known cost associated with mutual funds is the expense ratio. This represents the annual fee charged by the fund to cover operating expenses such as management fees, administrative costs, and marketing expenses. While expense ratios are disclosed upfront, many investors fail to consider their long-term impact. A fund with a seemingly small expense ratio of 1% can compound into a substantial cost over decades, significantly diminishing your overall returns.

For instance, if you invest ₹10,00,000 in a mutual fund with a 1% expense ratio and earn an average annual return of 8%, the compounded cost of the expense ratio over 20 years could amount to several lakhs. Lower expense ratio funds, such as passive index funds, offer a cost-efficient alternative to actively managed funds, where the higher fees often fail to justify the marginally better performance.

Exit Loads: The Cost of Early Withdrawal

Investors often overlook exit loads, which are charges levied by mutual funds when you redeem your units before a specified time frame. Typically ranging from 0.5% to 1%, exit loads are intended to discourage short-term trading and ensure that investors remain committed for the long term. However, if you need to withdraw your investment during unforeseen circumstances, these charges can eat into your returns.

Hidden Costs in the Background

Another invisible cost associated with mutual funds is transaction costs. These include brokerage fees, stamp duties, and Securities Transaction Tax (STT) incurred by the fund while buying or selling securities in its portfolio. Though these costs are not directly charged to investors, they are embedded in the fund’s Net Asset Value (NAV), indirectly lowering your returns.

Funds with high portfolio turnover—frequent buying and selling of securities—tend to have higher transaction costs. Actively managed funds, in particular, often incur significant transaction expenses, which can drag down their performance relative to low-turnover index funds.

Taxes: The Unavoidable Cost

Taxes represent yet another hidden cost of mutual funds. While taxes are a necessary obligation, their impact on mutual fund returns can be substantial if not managed effectively. Here’s how taxation applies to mutual funds:

- Equity Mutual Funds: Gains from equity funds held for less than 12 months are classified as short-term capital gains (STCG) and taxed at 15%. Gains from units held for more than 12 months are classified as long-term capital gains (LTCG), with gains exceeding ₹1 lakh taxed at 10% without indexation.

- Debt Mutual Funds: Gains from debt funds held for less than three years are treated as STCG and taxed at your applicable income tax slab rate. Gains from units held for more than three years qualify as LTCG, taxed at 20% with indexation benefits.

Taxation can significantly affect your mutual fund returns, especially if you frequently redeem units or fail to plan your investments with tax efficiency in mind.

Performance-Based Fees: An Additional Layer of Costs

Some mutual funds, particularly those managed by hedge fund-like structures or niche investment teams, impose performance-based fees in addition to the standard expense ratio. These fees are usually a percentage of the returns generated above a specified benchmark or “hurdle rate.”

While the idea of paying for performance may seem fair, it’s essential to evaluate whether the additional cost is justified by the returns delivered. For most investors, low-cost funds with straightforward fee structures provide a more predictable and cost-effective option.

Hidden Distribution Costs: Paying for Fund Sales

Many investors are unaware of the embedded distribution costs that mutual funds incur for marketing and selling their units. These costs are often labelled as “commissions” paid to distributors or advisors who recommend the fund to investors. While the commission itself is not directly charged to you, it forms part of the expense ratio, indirectly reducing your returns.

Direct plans, which eliminate intermediary commissions, offer a cost-effective alternative to regular plans. By investing in direct plans, you can save on distribution costs and enjoy higher returns over the long term.

Misaligned Incentives: Paying for Underperformance

One of the most frustrating hidden costs of mutual funds is the potential for misaligned incentives. Actively managed funds often charge high fees regardless of their performance, forcing investors to pay for subpar results. Over time, this can lead to significant wealth erosion, especially if you remain invested in a consistently underperforming fund.

It’s crucial to periodically review the performance of your mutual funds and switch to better-performing, low-cost alternatives when necessary. Don’t let inertia lock you into funds that fail to deliver value for money.

Opportunity Costs: The Impact of High Costs on Compounding

Finally, high mutual fund costs represent an opportunity cost in terms of foregone compounding. Every rupee spent on fees, taxes, or transaction costs is a rupee less available for reinvestment. Over decades, these hidden costs can compound into substantial amounts, depriving you of the full potential of your investments.

Example

A Tale of Sneha’s Mutual Fund Journey

Sneha, a young marketing professional from Mumbai , had recently started investing to secure her financial future. Like many first-time investors, she turned to mutual funds, lured by their promise of simplicity and professional management. After researching online and consulting her bank’s advisor, she decided to invest ₹5,00,000 in a popular equity mutual fund. The returns looked promising, and the advisor assured her it was a “safe” choice. Sneha was thrilled to finally take charge of her financial journey, but little did she know, a series of hidden costs were silently eroding her wealth.

The Expense Ratio Revelation

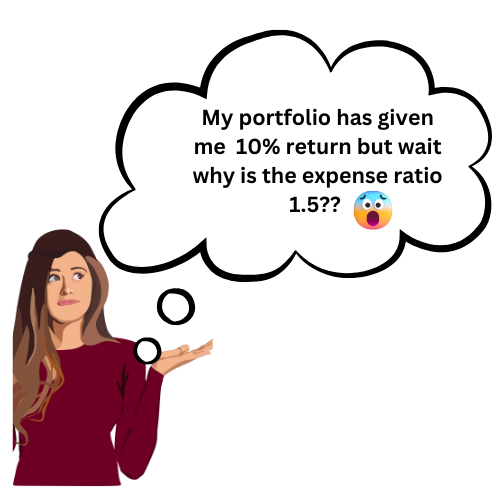

A year later, Sneha decided to review her investment performance. She noticed that her fund had delivered a decent return of 10%. But when she checked the fine print, she discovered the expense ratio of the fund was 1.5% annually. Initially, Sneha dismissed it as a minor fee, but out of curiosity, she did the math.

Her ₹5,00,000 investment had grown to ₹5,50,000 before expenses. However, 1.5% of the total amount—₹8,250—was deducted as the expense ratio. Over the course of 20 years, Sneha realized, this seemingly small percentage could compound into a significant amount, eating into her returns. She started exploring funds with lower expense ratios, such as index funds, and regretted not paying attention to this detail earlier.

The Exit Load Surprise

Life threw Sneha a curveball when she needed to withdraw a portion of her investment to cover unexpected medical expenses. She redeemed ₹1,00,000 from her mutual fund, only to discover that an exit load of 1% was deducted since she had withdrawn within the first year. This meant she received ₹99,000 instead of the full amount.

Sneha couldn’t help but feel frustrated. She had invested her hard-earned money, only to face a penalty for accessing it when she needed it most. Moving forward, she made a note to consider funds with lower or no exit loads and to understand the lock-in periods before investing.

The Hidden Transaction Costs

Over time, Sneha noticed that her fund’s Net Asset Value (NAV) didn’t always align with her expectations. Despite market growth, her returns seemed slightly lower than anticipated. Upon digging deeper, she learned about the transaction costs incurred by mutual funds.

Her fund had a high portfolio turnover, meaning the fund manager frequently bought and sold stocks to adjust the portfolio. Each transaction incurred brokerage fees and taxes, which were deducted from the fund’s overall returns. These costs weren’t directly visible to Sneha but were quietly embedded in the NAV. She realized that funds with a lower turnover rate might be a better fit for her investment strategy.

Taxes: The Unavoidable Bite

After three years, Sneha sold another portion of her mutual fund investment to fund her sister’s wedding. She was delighted to see substantial long-term gains but soon learned that a portion of these gains would be subject to taxation. The long-term capital gains (LTCG) tax on equity mutual funds—10% on gains above ₹1,00,000—meant she had to part with ₹3,000 in taxes.

Though taxes are inevitable, Sneha understood the importance of factoring them into her investment calculations. She started planning her withdrawals more strategically, aiming to minimize tax liabilities while maximizing her returns.

The Performance Fee Dilemma

Encouraged by her friends, Sneha also explored a niche mutual fund that promised exceptional returns. This fund had a performance-based fee structure, charging an additional fee if returns exceeded 12% annually. While the fund performed well initially, it struggled to sustain its momentum in subsequent years. Yet, the high fees continued to eat into her profits.

Sneha learned an important lesson: higher costs don’t always translate into higher returns. She decided to stick with low-cost funds where the fee structures were simpler and more predictable.

Direct Plans vs Regular Plans

During a casual chat with her colleague Ramesh, Sneha discovered she had been investing in regular mutual fund plans, which included commissions paid to distributors. Ramesh explained that direct plans of mutual funds eliminate these commissions, allowing investors to save on costs and enjoy better returns.

Sneha promptly switched her investments to direct plans. Over the next few years, she saw a noticeable improvement in her returns, simply by avoiding the unnecessary distribution costs embedded in regular plans.

Opportunity Costs of High Fees

Finally, Sneha realized the true opportunity cost of hidden fees. Had she opted for low-cost index funds from the beginning, she could have reinvested the savings from lower fees into additional investments. Over decades, this reinvestment could have compounded into a significant amount.

For instance, by saving ₹5,000 annually on fees and reinvesting it at an 8% annual return, Sneha could have accumulated nearly ₹10,00,000 over 30 years. This realization motivated her to optimize her portfolio and take a more cost-conscious approach to investing.

The Takeaway

Sneha’s journey with mutual funds was a mix of ups and downs, filled with valuable lessons about the hidden costs of investing. From expense ratios to taxes and performance fees, each layer of costs taught her the importance of due diligence and informed decision-making.

Today, Sneha is a more confident and savvy investor. She carefully evaluates fund costs, opts for direct plans, and prioritizes low-cost, high-value investments. Her story serves as a reminder to all investors: don’t let hidden costs erode your wealth. Take the time to understand where your money is going, and make every rupee count.

Conclusion

While mutual funds remain an excellent investment vehicle for many, it’s essential to be aware of the hidden costs that can erode your returns. By understanding expense ratios, exit loads, transaction costs, taxes, and other fees, you can make informed decisions and optimize your investment portfolio. Opt for low-cost funds, invest in direct plans, and periodically review your fund performance to ensure that you’re not paying more than you think.