As we enter the financial year 2025-26, numerous new regulations, policies, and updates come into effect, bringing changes that impact individuals and businesses across India. These financial changes, updates, announced in the Union Budget 2025 and various government directives, aim to promote economic growth, enhance financial security, and provide relief to taxpayers. Staying informed about these changes is crucial to making the most of the new financial landscape.

Key Financial Changes Effective from 1st April 2025 are as follows :

Revised Income Tax Slabs

One of the most significant changes is the revision of income tax slabs under the new tax regime. The government has introduced a progressive tax structure with increased thresholds, providing substantial relief to taxpayers. The revised income tax slabs for the financial year 2025-26 are as follows:

Income Range (₹) | Tax Rate (%) |

0 – 4,00,000 | Nil |

4,00,001 – 8,00,000 | 5% |

8,00,001 – 12,00,000 | 10% |

12,00,001 – 16,00,000 | 15% |

16,00,001 – 20,00,000 | 20% |

20,00,001 – 24,00,000 | 25% |

Above 24,00,000 | 30% |

Under the new tax regime, individuals earning up to ₹12 lakh annually are exempt from paying income tax due to a rebate under Section 87A. For salaried individuals, the standard deduction of ₹75,000 further increases the tax-free income threshold to ₹12.75 lakh. These changes aim to alleviate financial stress for taxpayers while stimulating consumption and investment.

Unified Pension Scheme for Government Employees

The Unified Pension Scheme replaces the Old Pension Scheme and provides enhanced benefits for eligible government employees. Employees with a minimum of 25 years of service are entitled to a pension equivalent to 50% of their last 12 months’ average basic salary. Payouts are inflation-adjusted, ensuring retirees’ financial security in the long term. This scheme reflects the government’s commitment to supporting its workforce even after retirement.

The National Payments Corporation of India (NPCI) has introduced new regulations for Unified Payments Interface (UPI) transactions, effective April 1, 2025. These changes aim to enhance security, improve interoperability, and provide a seamless user experience. Here are the key updates:

- Deactivation of Inactive Mobile Numbers: UPI IDs linked to inactive mobile numbers will be deactivated. This measure ensures that recycled or reassigned mobile numbers do not lead to unauthorized access or transaction errors. Users must keep their registered mobile numbers active and updated with their banks to avoid disruptions in UPI services.

- Weekly Database Updates: Banks and Payment Service Providers (PSPs) are now required to update their databases weekly using the Mobile Number Revocation List (MNRL) and Digital Intelligence Platform (DIP). This step minimizes errors caused by mobile number churn, where previously assigned numbers are reallocated to new users.

- Explicit User Consent for UPI Number Seeding: UPI apps must obtain explicit user consent before seeding or porting a UPI number. The consent mechanism now requires users to opt in manually, ensuring transparency and preventing misleading or forceful messaging. Consent cannot be sought during or before a transaction, reinforcing user control over their data.

- Removal of the “Collect Payments” Feature: To combat fraud, the “Collect Payments” feature is now restricted to large, verified merchants. For person-to-person transactions, a limit of ₹2,000 has been set. This change aims to reduce misuse of the pull-payment system while maintaining its utility for legitimate purposes.

- Numeric UPI IDs: UPI applications will now offer numeric UPI IDs, but users must actively choose to enable this feature. By default, numeric UPI IDs are opted out, and users need to provide explicit permission to activate them. This ensures that users have full control over their UPI settings.

- Monthly Reporting by PSPs: Payment Service Providers (PSPs) must report cases where they locally resolve UPI numbers due to delays in NPCI’s system responses. This monthly reporting ensures transparency and accountability, driving improvements in the UPI ecosystem.

- Impact on Users: Users who fail to update their mobile numbers with their banks or UPI apps may face issues such as:

- Loss of access to UPI accounts if their number has been reassigned.

- Failed or misdirected transactions.

- Delayed resolution of discrepancies related to UPI numbers.

- Steps for Users to Avoid Disruptions:

- Ensure that your registered mobile number is active and updated with your bank and UPI apps.

- Regularly check for consent requests in your UPI apps and manually opt in if required.

- Avoid ignoring UPI-related notifications from your bank or PSP app.

These updates reflect NPCI’s commitment to making UPI transactions more secure and efficient. By addressing issues such as mobile number churn and enhancing user consent mechanisms, these guidelines aim to build trust and reliability in the digital payments ecosystem.

The Goods and Services Tax (GST) portal has introduced Multi-Factor Authentication (MFA) for accessing accounts, improving security for taxpayers. Additionally, e-Way Bills can only be generated for base documents issued within the last 180 days, streamlining compliance and reducing documentation errors. These updates highlight the government’s focus on simplifying the tax framework while maintaining its integrity.

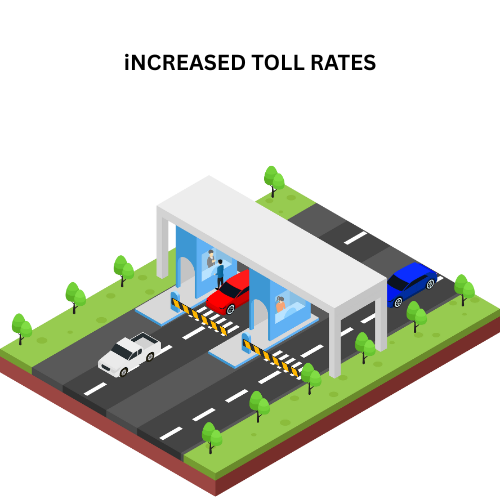

Increase in Toll Rates

Transportation costs are set to rise as toll rates on national highways see an approximate increase of 3%. Light vehicles face hikes of ₹5-₹10 per trip, while heavy vehicles see increases of ₹20-₹25 per trip. These increased rates will generate additional funds for infrastructure development but may require adjustments for regular commuters and logistics companies.

Changes in LPG and Essential Medicine Prices

The cost of a 19 kg commercial LPG cylinder has been reduced by ₹41, benefiting small businesses and food outlets. Meanwhile, essential medicines such as painkillers and antibiotics have increased in price by 4% due to rising production costs. Consumers should plan their budgets accordingly to accommodate these changes.

Higher TDS Thresholds

The Tax Deducted at Source (TDS) thresholds for various commissions have been increased. Insurance commission thresholds rise from ₹15,000 to ₹20,000, while interest income thresholds for non-senior citizens increase from ₹40,000 to ₹50,000. These updates provide greater financial flexibility to taxpayers and incentivize savings and investments.

Stricter KYC Norms

Banks and financial institutions have implemented stricter Know Your Customer (KYC) norms to improve security and prevent fraudulent activity. Customers are urged to update their KYC details promptly to avoid any disruptions in banking services. This move is part of broader efforts to fortify the financial system’s resilience.

Positive Impact on Investors

Investors in equities and mutual funds stand to benefit from the increased TDS threshold on dividend income. By retaining more of their earnings, they are incentivized to participate in the financial markets more actively. Additionally, reforms aimed at improving security and compliance underscore the government’s commitment to building a robust financial ecosystem.

Conclusion

The financial changes effective from April 1, 2025, bring both opportunities and challenges. From tax relief and pension enhancements to stricter regulations for digital transactions and updates to GST compliance measures, these reforms aim to promote growth and stability. Individuals and businesses alike must stay proactive and informed to leverage these changes effectively and manage their finances wisely. The new policies mark a step forward in building a resilient and inclusive financial framework that benefits all stakeholders.