4.1 Forward Contract

A forward contract, sometimes abbreviated as “forward,” is an agreement to buy or sell an asset at a predetermined price on a future point. It is a customized OTC contract between two parties, where settlement takes place on a specific date in the future at today’s pre-agreed price. These contracts are not standardized or regulated by any third-party authority and are considered a type of over the counter (OTC) deal between the two parties.

Forward contracts are an excellent tool for hedging your investments. They can also be used for speculations, but that option is less popular due to their non-standardized, non-regulated nature. The basic purpose of these contracts is to protect against prospective losses. They offer the ability to lock in a price for the future. This guaranteed price might be critical, especially in businesses where prices are prone to severe volatility.

Example of Currency Forward Contract

The currency is traded on a future date is a foreign exchange market. The exchange rate is locked at the time of signing the contract, and hence, market fluctuations don’t have an impact on it. Unlike other derivatives like the exchange-traded currency futures, parties can customize a currency forward contract to suit their needs.

Example: A company X in the UK imports oil worth 1 million Euros from company Y in the USA. As per their deal, company X has to pay the amount within 90 days of delivery. Let us assume that the current exchange rate is 1 Euro equals 1.2 USD. So the exporter Y in the USA expects USD 1.2 million within the 90 days of delivery.

However, the currency exchange rates are volatile and may increase or decrease in the next 90 days. The exporter wants to insulate himself from such risks, hence enters into a currency forward deal with a bank. The bank offers an exchange rate of 1.19 on the 90th day, which is slightly less than the current rate. The company Y receives 1 million Euro on the 90th day from company X and deposits it to the bank. The bank applies the locked exchange rate of 1.19 and gives them $1.19 million, irrespective of the current exchange rate. If the rate tips below the locked limit, the bank suffers a loss, and the exporter successfully evades it. If the rate goes above the locked limit, the exporter misses out on the opportunity while banks book a profit.

4.2 Future Contract

A futures contract is a standardized contract, traded on an exchange, to buy or sell a certain underlying asset or an instrument at a certain date in the future, at a specified price. The currency futures contract provides for the future delivery of a specified amount of a foreign currency at a particular date, time, and place. Fulfillment of a contract, depending on whether one is a buyer or seller, is satisfied by accepting or by making delivery of the specified currency on the value date of the contract. A buy or sell position can also be closed out by making an offsetting purchase or sale of an equivalent contract prior to the expiration of trading for the contract.

A futures contract is a standardized contract, traded on an exchange, to buy or sell a certain underlying asset or an instrument at a certain date in the future, at a specified price. The currency futures contract provides for the future delivery of a specified amount of a foreign currency at a particular date, time, and place. Fulfillment of a contract, depending on whether one is a buyer or seller, is satisfied by accepting or by making delivery of the specified currency on the value date of the contract. A buy or sell position can also be closed out by making an offsetting purchase or sale of an equivalent contract prior to the expiration of trading for the contract.

They are highly regulated, and any counterparty still holding the contract at the expiration date is legally bound to take delivery of the currency on the given date and at the given price.

Based on the type of currency traded and the contract size, a currency futures contract can be of several types. The most commonly traded currencies are Euro, US Dollar, Canadian Dollar, Pound, Franc, and Yen. Depending upon size, they can be standard or full-sized, mini or half-sized, and micro (about a tenth of the standard).

Currency futures are a linear product, and calculating profits or losses on these instruments is similar to calculating profits or losses on Index futures. In determining profits and losses in futures trading, it is essential to know both the contract size (the number of currency units being traded) and also the “tick” value.

A tick is the minimum size of price change. The market price will change only in multiples of the tick. Tick values differ for different currency pairs and different underlyings. For e.g. in the case of the USDINR currency futures contract the tick size shall be 0.25 paise or 0.0025 Rupee. To demonstrate how a move of one tick affects the price, imagine a trader buys a contract (USD 1000 being the value of each contract) at Rs. 44.7500. One tick move on this contract will translate to Rs.44.7475 or Rs.44.7525 depending on the direction of market movement. The contract amount (or “market lot”) is the minimum amount that can be traded. Therefore, the profit/loss associated with change of one tick is: tick x contract amount The value of one tick on each USDINR contract is Rupees 2.50 (1000 X 0.0025). So if a trader buys 5 contracts and the price moves up by 4 ticks, he makes Rupees 50.00 (= 5 X 4 X 2.5).

4.3 Distinction Between Futures And Forward Contracts

Forward contracts are often confused with futures contracts. The confusion is primarily because both serve essentially the same economic functions of allocating risk in the probability of future price uncertainty. However futures have some distinct advantages over forward contracts as they eliminate counterparty risk and offer more liquidity and price transparency. However, it should be noted that forwards enjoy the benefit of being customized to meet specific client requirements. The advantages and limitations of futures contracts are as follows:

Forward contracts are often confused with futures contracts. The confusion is primarily because both serve essentially the same economic functions of allocating risk in the probability of future price uncertainty. However futures have some distinct advantages over forward contracts as they eliminate counterparty risk and offer more liquidity and price transparency. However, it should be noted that forwards enjoy the benefit of being customized to meet specific client requirements. The advantages and limitations of futures contracts are as follows:

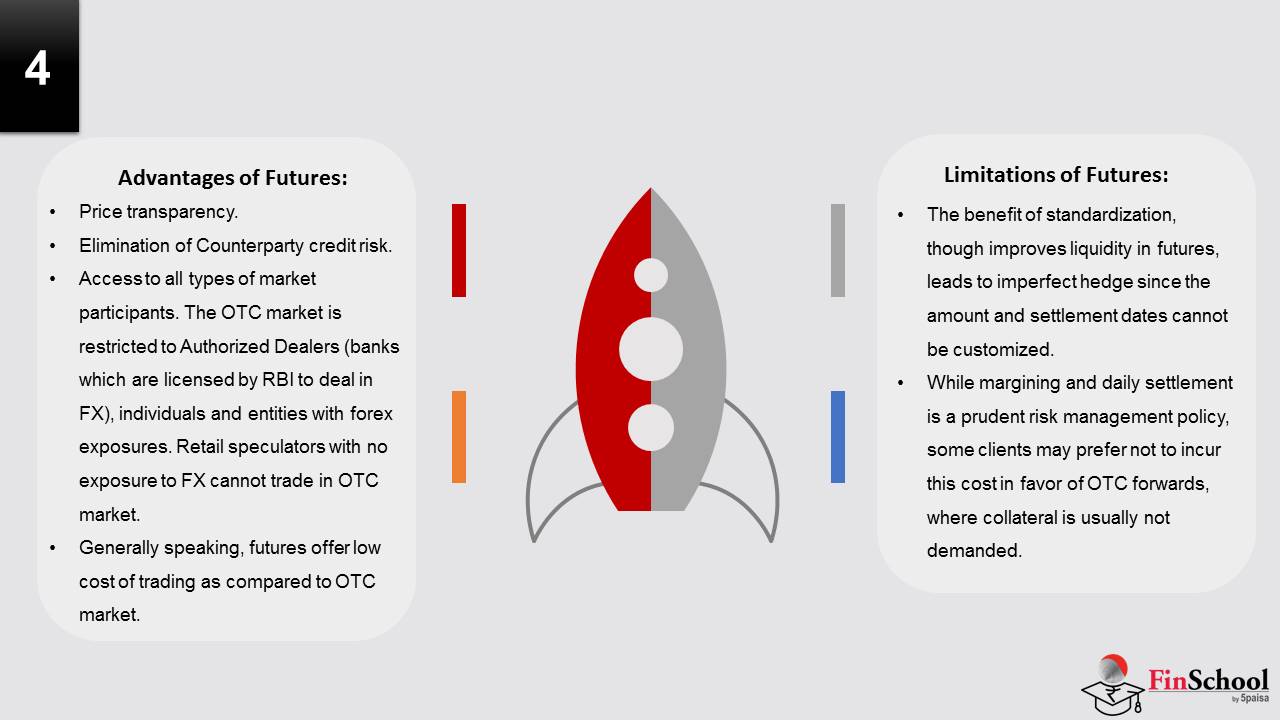

Advantages of Futures:

- Price transparency.

- Elimination of Counterparty credit risk.

- Access to all types of market participants. The OTC market is restricted to Authorized Dealers (banks which are licensed by RBI to deal in FX), individuals and entities with forex exposures. Retail speculators with no exposure to FX cannot trade in OTC market.

- Generally speaking, futures offer low cost of trading as compared to OTC market.

Limitations of Futures:

- The benefit of standardization, though improves liquidity in futures, leads to imperfect hedge since the amount and settlement dates cannot be customized.

- While margining and daily settlement is a prudent risk management policy, some clients may prefer not to incur this cost in favor of OTC forwards, where collateral is usually not demanded.

4.4 Interest Rate Parity And Pricing Of Currency Futures

Let us assume that risk free interest rate for one year deposit in India is 7% and in USA it is 3%. You as smart trader/ investor will raise money from USA and deploy it in India and try to capture the arbitrage of 4%. You could continue to do so and make this transaction as a non ending money making machine. Life is not that simple! And such arbitrages do not exist for very long.

Let us assume that risk free interest rate for one year deposit in India is 7% and in USA it is 3%. You as smart trader/ investor will raise money from USA and deploy it in India and try to capture the arbitrage of 4%. You could continue to do so and make this transaction as a non ending money making machine. Life is not that simple! And such arbitrages do not exist for very long.

We will carry out the above transaction through an example to explain the concept of interest rate parity and derivation of future prices which ensure that arbitrage does not exist.

Assumptions:

- Spot exchange rate of USDINR is 50 (S)

- One year future rate for USDINR is F

- Risk free interest rate for one year in USA is 3% (RUSD

- Risk free interest rate for one year in India is 7% (R ) INR

- Money can be transferred easily from one country into another without any restriction of amount, without any taxes etc)

You decide to borrow one USD from USA for one year, bring it to India, convert it in INR and deposit for one year in India. After one year, you return the money back to USA.

On start of this transaction, you borrow 1 USD in US at the rate of 3% and agree to return 1.03 USD after one year (including interest of 3 cents). This 1 USD is converted into INR at the prevailing spot rate of 50. You deposit the resulting INR 50 for one year at interest rate of 7%. At the end of one year, you receive INR 3.5 (7% of 50) as interest on your deposit and also get back your principal of INR 50 i.e., you receive a total of INR 53.5. You need to use these proceeds to repay the loan taken in USA.

Two important things to think before we proceed:

- The loan taken in USA was in USD and currently you have INR. Therefore you need to convert INR into USD

- What exchange rate do you use to convert INR into USD?

At the beginning of the transaction, you would lock the conversion rate of INR into USD using one year future price of USDINR. To ensure that the transaction does not result into any risk free profit, the money which you receive in India after one year should be equal to the loan amount that you have to pay in USA.

We will convert the above argument into a formula: S(1+RINR)= F(1+RUSD) Or, F/ S = (1+RINR) / (1+RUSD) Another way to illustrate the concept is to think that the INR 53.5 received after one year in India should be equal to USD 1.03 when converted using one year future exchange rate. Therefore, F/ 50 = (1+.07) / (1+.03)

F= 51.9417 Approximately, F is equal to the interest rate difference between two currencies i.e., F = S + (RINR- RUSD)*S

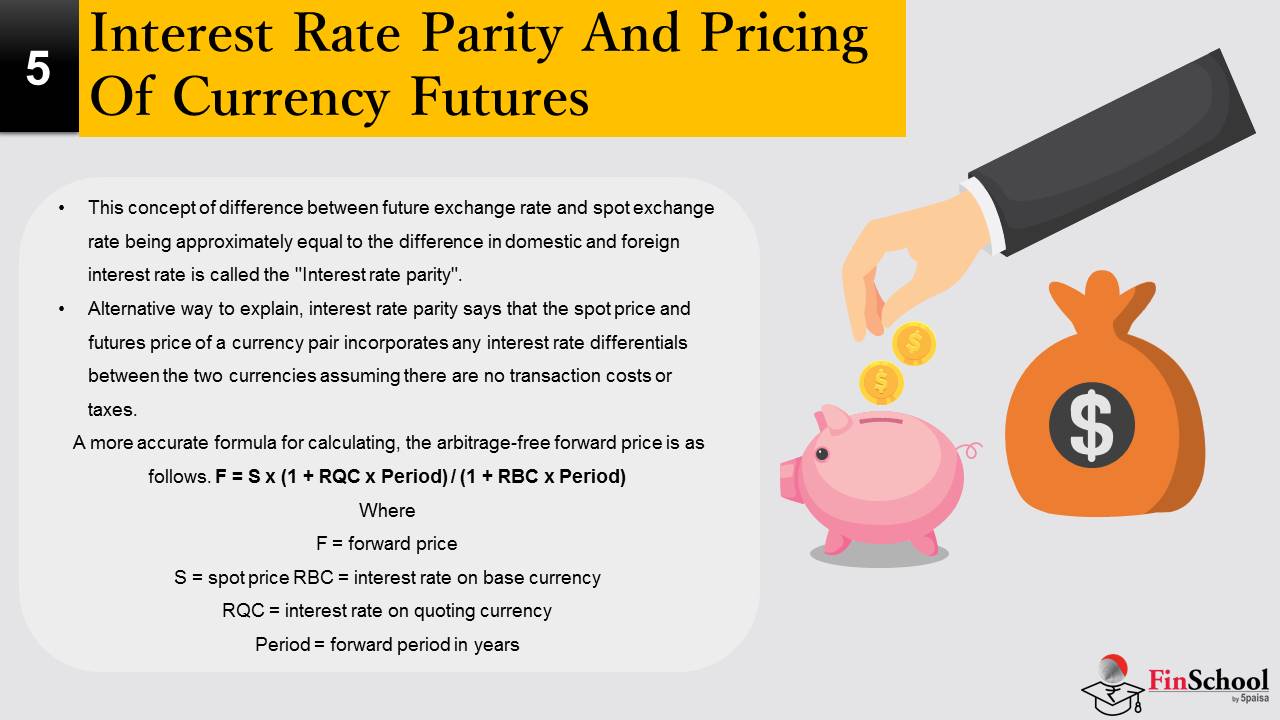

This concept of difference between future exchange rate and spot exchange rate being approximately equal to the difference in domestic and foreign interest rate is called the “Interest rate parity”.

Alternative way to explain, interest rate parity says that the spot price and futures price of a currency pair incorporates any interest rate differentials between the two currencies assuming there are no transaction costs or taxes. A more accurate formula for calculating, the arbitrage-free forward price is as follows. F = S x (1 + RQC x Period) / (1 + RBC x Period)

Where

F = forward price

S = spot price RBC = interest rate on base currency

RQC = interest rate on quoting currency

Period = forward period in years

For a quick estimate of forward premium, following formula mentioned above for USDINR currency pair could be used. The formula is generalized for other currency pair and is given below: F = S + (S x (RQC – RBC) x Period)

In above example, if USD interest rate were to go up and INR interest rate were to remain at 7%, the one year future price of USDINR would decline as the interest rate difference between the two currencies has narrowed and vice versa.

Traders use expectation on change in interest rate to initiate long/ short positions in currency futures. Everything else remaining the same, if USD interest rate is expected to go up (say from 2.5% to 3.0%) and INR interest rate are expected to remain constant say at 7%; a trader would initiate a short position in USDINR futures market.

Illustration:

Suppose 6 month interest rate in India is 5% (or 10% per annum) and in USA are 1% (2% per annum). The current USDINR spot rate is 50. What is the likely 6 month USDINR futures price? As explained above, as per interest rate parity, future rate is equal to the interest rate differential between two currency pairs. Therefore approximately 6 month future rate would be:

Spot + 6 month interest difference = 50 + 4% of 50 = 50 + 2 = 52The exact rate could be calculated using the formula mentioned above and the answer comes to

51.98. 51.98 = 50 x (1+0.1/12 x 6) / (1+0.02/12 x 6)

Concept of premium and discount

Therefore one year future price of USDINR pair is 51.94 when spot price is 50. It means that INR is at discount to USD and USD is at premium to INR. Intuitively to understand why INR is called at discount to USD, think that to buy same 1 USD you had to pay INR 50 and you have to pay 51.94 after one year i.e., you have to pay more INR to buy same 1 USD. And therefore future value of INR is at discount to USD. Therefore in any currency pair, future value of a currency with high interest rate is at a discount (in relation to spot price) to the currency with low interest rate.